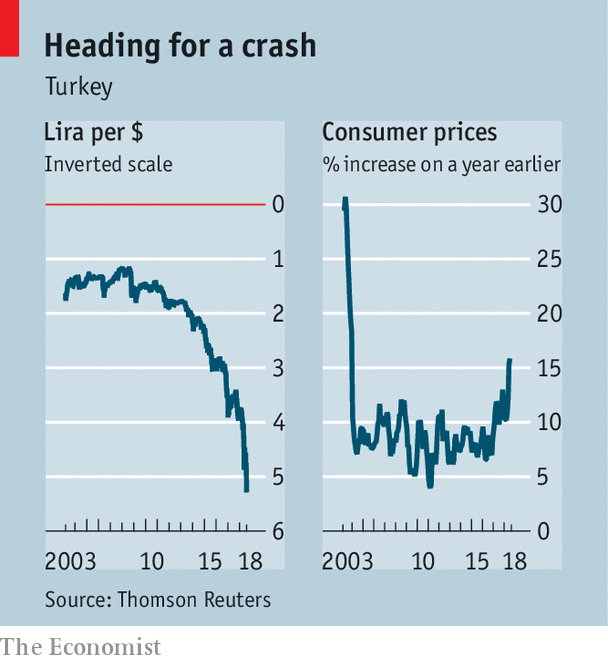

There is little evidence that Turkish President Recep Tayyip Erdogan is going to back down from his confrontation with the US. He gave three speeches on Sunday and he essentially shut down all possibles avenues for compromise. According to Bloomberg:

“In three public addresses, Erdogan lashed out at the United States, threatening to find new alliances and new markets. He also took higher interest rates off the table and said Turkey wouldn’t accept an international bailout. His message was essentially the opposite of what investors have called for to stem the plunge in the markets.”

In an op-ed published by The New York Times, Erdogan wrote:

“At a time when evil continues to lurk around the world, unilateral actions against Turkey by the United States, our ally of decades, will only serve to undermine American interests and security. Before it is too late, Washington must give up the misguided notion that our relationship can be asymmetrical and come to terms with the fact that Turkey has alternatives. Failure to reverse this trend of unilateralism and disrespect will require us to start looking for new friends and allies.”

The threat to the unity of NATO is unmistakable and there are countries in the region–notably Russia and Iran–who will seek to exploit this fissure. Erdogan also indicated that Turkey would be willing to trade with its other major trading partners in local currencies and not use the dollar, echoing rising sentiments in many other countries to stop using the dollar as a reserve currency. If a sufficient number of other countries stop using the dollar for international transactions, the US will find that the dollar will be subjected to pressures that will constrain US control over its interest rates, its budgets, and its bonds. The financial markets will be watching closely to see if the instability in Turkey spreads to major banks and, from the, to other emerging markets.

Russia, Kazakhstan, Iran, Turkmenistan and Azerbaijan have signed an agreement on how to share the resources of the Caspian Sea, the world’s largest inland lake. In 2013 The US Energy Information Agency assessed the oil and nautral gas potential of the Caspian Sea:

“EIA estimates that there were 48 billion barrels of oil and 292 trillion cubic feet (Tcf) of natural gas in proved and probable reserves within the basins that make up the Caspian Sea and surrounding area in 2012. Offshore fields account for 41% of total Caspian crude oil and lease condensate (19.6 billion barrels) and 36% of natural gas (106 Tcf). In general, most of the offshore oil reserves are in the northern part of the Caspian Sea, while most of the offshore natural gas reserves are in the southern part of the Caspian Sea.

“In addition, the U.S. Geological Survey (USGS) estimates another 20 billion barrels of oil and 243 Tcf of natural gas in as yet undiscovered, technically recoverable resources. Much of this is located in the South Caspian Basin, where territorial disputes over offshore waters hinder exploration.”

Negotiations over the resources have been going on for almost three decades, and this agreement represents a turning point in the relations of the countries abutting the Sea. Iran has also reached agreement with China to develop the South Pars Gas field, the world’s largest natural gas reservoir. China will take over the role of the French oil company Total, which had the rights to develop the field but stopped working on the gas field because of the sanctions on Iran. Bloomberg describes the new deal:

“China National Petroleum Corp. is expected to take the lead on a $5 billion project to develop Iran’s share of the world’s biggest gas deposit, taking over from France’s Total SA, which halted operations after U.S. President Donald Trump reimposed sanctions on the Islamic Republic.

“State-owned CNPC, which joined a consortium with Total and Iran’s Petropars Ltd. in 2016 to develop Phase 11 of the South Pars Gas field, is set to increase its stake in the project from the current 30 percent. Total had originally agreed to take a 50.1 percent interest.”

There are two relevant points to make about these agreements. First, it seems clear that many countries are willing to work with Iran despite the US insistence that all economic ties with Iran be terminated. We will have to see how the Trump Administration responds to these acts of defiance. Second, all of the countries are highly dependent on oil and gas revenues and one can expect them to develop these fossil fuels as quickly as possible. In a world faced with climate change brought about by greenhouse gas emissions, the last thing it needed was for more oil and natural gas become available for consumption. Agreements to limit greenhouse gas emissions will likely become more difficult.

{kind=link}

{kind=link}

{kind=link}

Leave a comment